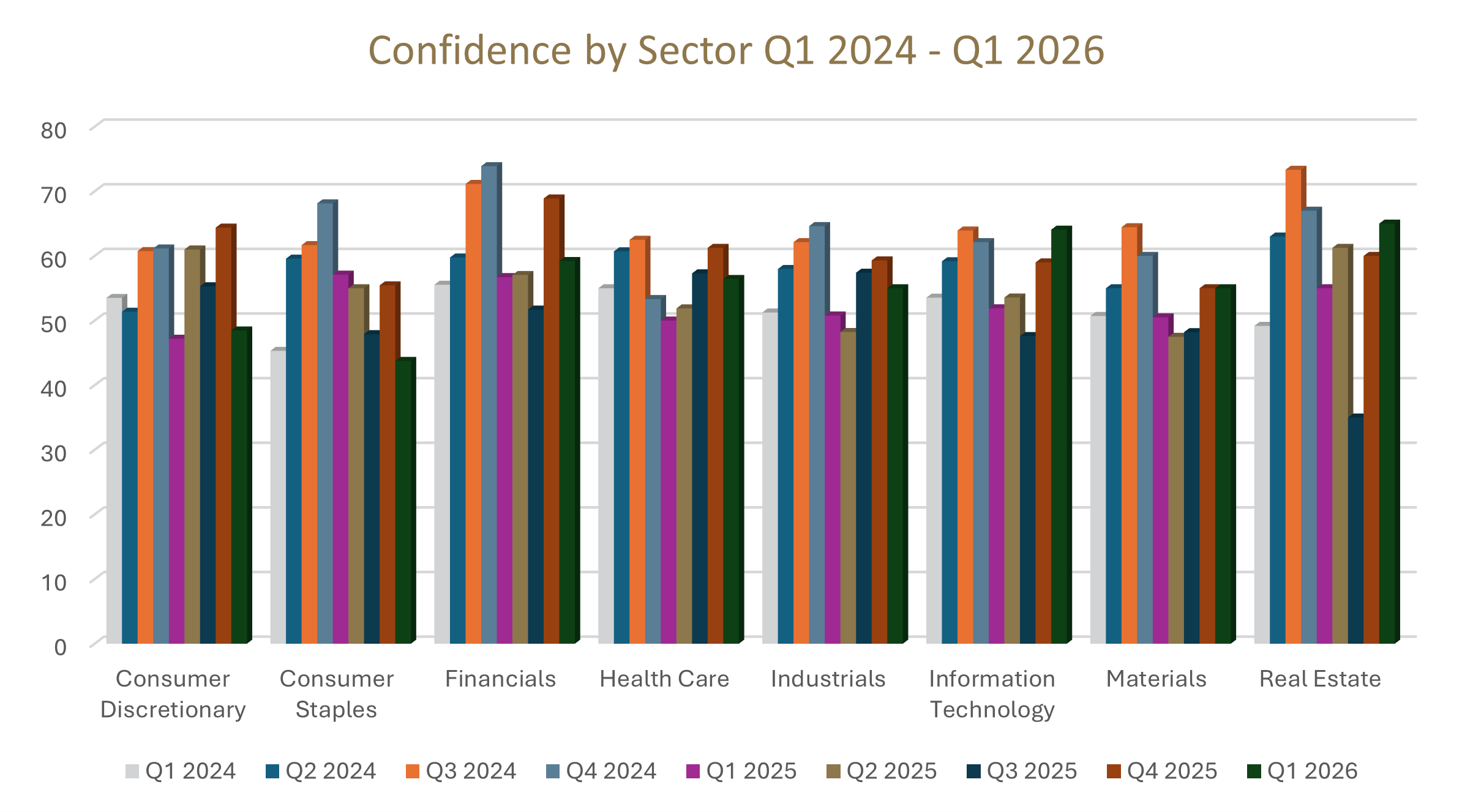

Information Technology (64.1, +5.1 points)

Confidence driver: AI adoption accelerating across productivity and operations

Investment stance: Strong appetite for digital transformation and automation

Cost pressure: Skills shortages persist; hardware/software costs stable

Policy exposure: Broadly positive on infrastructure investment commitments

Risk outlook: Middle East conflict impact on global tech supply chains monitored

Utilities (61.25, +0.25 points)

Confidence driver: Improved infrastructure investment and regulatory stability

Investment stance: Cautiously optimistic; long-term capex planned

Cost pressure: Fuel price volatility threatens operational margins

Policy exposure: High; depends on budget execution and SOE reform

Risk outlook: Municipal capacity constraints and geopolitical fuel shocks

Financials (59.2, −9.7 points)

Confidence driver: Fiscal discipline welcomed; credit conditions stable

Investment stance: Selective; watching political risk and policy certainty

Cost pressure: Rising compliance costs; BEE regulations a drag

Policy exposure: Highly sensitive to tax policy and economic growth trajectory

Risk outlook: Political fragmentation and fuel-driven inflation

Health Care (56.4, −4.9 points)

Confidence driver: GNU stability; demand for health services resilient

Investment stance: Moderate; innovation ongoing

Cost pressure: Input costs stabilising; margins under pressure

Policy exposure: Trump USAID funding cuts impacting NGO-linked sectors

Risk outlook: Oil price impact on pharmaceutical and logistics costs

Industrials (55.0, −4.3 points)

Confidence driver: Infrastructure budget allocations; Transnet and Eskom improvements

Investment stance: Selective expansion; waiting for policy clarity

Cost pressure: Fuel, transport, and logistics costs elevated

Policy exposure: High; red tape, BEE compliance, and municipal rates cited

Risk outlook: Geopolitical fuel shocks and US trade policy uncertainty

Materials (55.0, 0 points)

Confidence driver: Commodity price stabilisation; export opportunities

Investment stance: Hold; watching global demand signals

Cost pressure: Elevated on transport and energy

Policy exposure: Moderate; Transnet and Eskom reforms critical

Risk outlook: Global market volatility; Middle East tensions affecting demand

Consumer Discretionary (48.5, −15.9 points)

Confidence driver: Weak; disposable income under pressure from inflation and tax bracket creep

Investment stance: Cautious; demand outlook subdued

Cost pressure: High; fuel, input costs, and margin compression

Policy exposure: Budget measures on discretionary spend watched closely

Risk outlook: Trump trade policy and Middle East war impact on sentiment

Consumer Staples (43.75, −11.75 points)

Confidence driver: Weakest sector; demand muted, input costs elevated

Investment stance: Defensive; efficiency focus

Cost pressure: Severe; fuel, logistics, and commodity input pressures

Policy exposure: Limited confidence in policy materialisation

Risk outlook: Iran-driven fuel price hikes and geopolitical alliances damaging trade