IT M&A markets have bifurcated sharply. Businesses with contracted, annuity-based income are transacting at multiples that reflect genuine scarcity value. Project dependent and time-and-materials businesses face meaningful compression, regardless of absolute profitability. That gap is structural, not cyclical, and it is now firmly embedded in how both strategic acquirers and private equity underwrite IT transactions. Understanding where your business sits on that spectrum, and what moves the needle before a process, is the most valuable analysis an IT business owner can do ahead of a sale.

What Acquirers Actually Mean by Recurring Revenue

The term is used loosely, and that looseness has real consequences in due diligence. Recurring revenue, in buyer terms, is income that is contractually obligated to recur, measurable in advance, and defensible under scrutiny. An MSP on three year agreements with documented churn below 5% is a fundamentally different asset to one with the same top line on rolling 30 day arrangements. Buyers usually value that difference at 2x to 4x EBITDA multiples.

Most acquirers apply a three tier framework: fully contracted recurring (MRR/ARR under multi-year agreements); quasi-recurring (high-probability repeat without contractual obligation); and transactional (project, T&M, one-off). Only the first tier receives full credit in an EV/Revenue or EV/ARR multiple. The second attracts a partial discount. The third is valued on EBITDA alone, at a meaningful discount to contracted peers.

The Multiple Gap: What the Data Shows

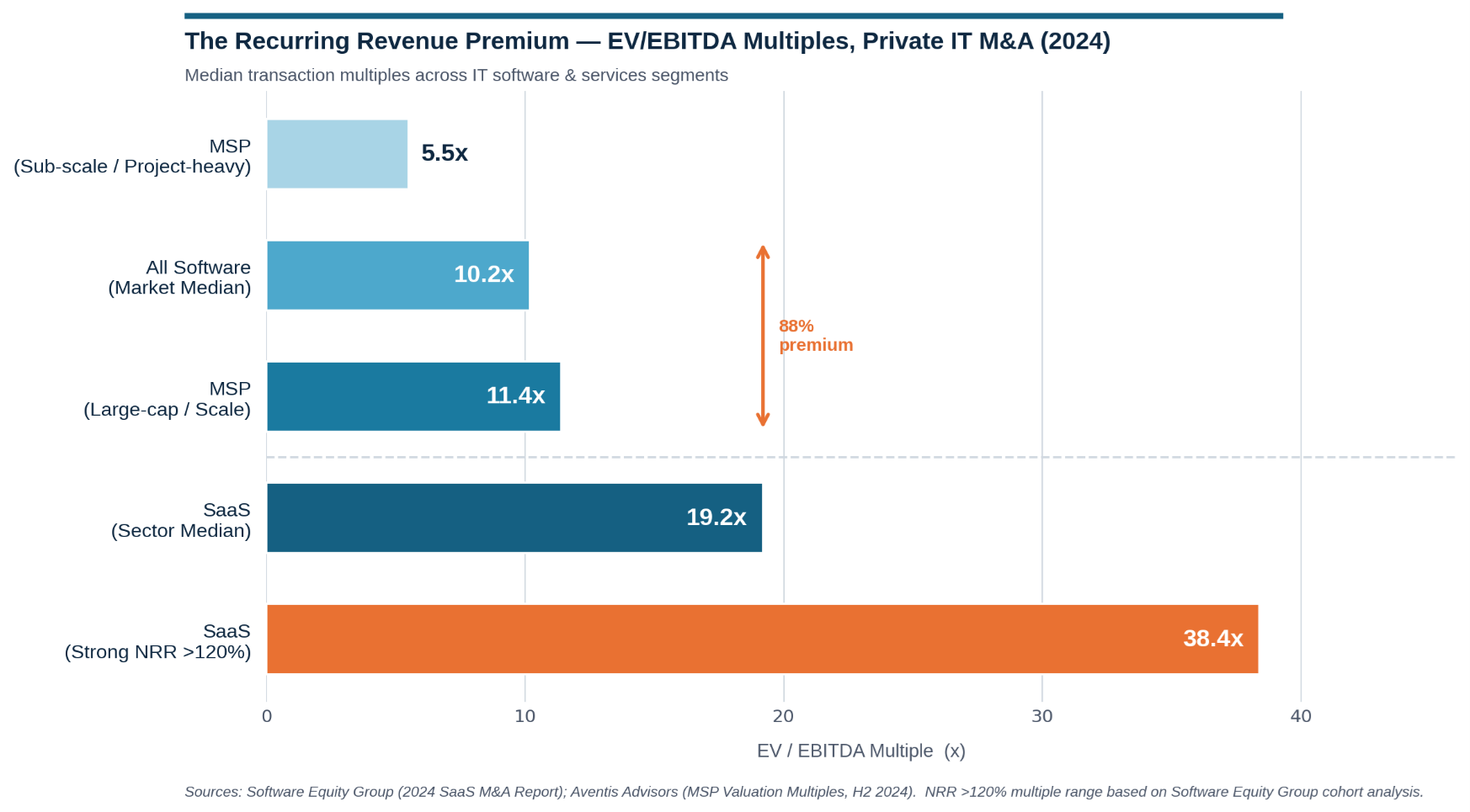

Across 3,183 private software transactions in 2024, SaaS businesses achieved a median EV/EBITDA of 19.2x, an 88% premium over the 10.2x median for all software deals (Software Equity Group). MSPs at scale are achieving 9–12x EBITDA; sub-scale or project heavy peers typically clear 5–6x on identical profitability. The gap is almost entirely

explained by recurring revenue composition. Two structural factors drive it:

- Underwriting certainty. For PE sponsors underwriting returns over a 3-5 year hold, anchoring the investment thesis to visible recurring revenue is not a preference, it is an investment committee prerequisite. NRR above 120% can more than double the achievable multiple versus sector median (Software Equity Group, 2024); churn above 10% annually compresses multiples by 1–3x.

- Competitive process dynamics. Recurring revenue assets attract both financial and strategic buyers simultaneously, the single most reliable driver of price tension in a sell-side process. Project-heavy businesses attract a narrower buyer universe and rarely generate the same competitive tension at close.

Key Levers Before Entering a Sell-Side Process

- Formalise contracts. Rolling or informal agreements consistently provide a recurring discount, independent of past renewal patterns. Multi-year agreements averaging more than 24 months can lift multiples by approximately 1x in isolation.

- Clean your revenue reporting. MRR and ARR must be calculated consistently and separated clearly from project revenue. Buyers disaggregate this in due-diligence regardless, presenting it cleanly prevents value erosion through ambiguity and accelerates exclusivity.

- Track NRR and manage concentration. 28% of SaaS CEOs still do not track gross revenue retention consistently (Software Equity Group), a blind spot that surfaces in diligence and compresses multiples. Customer concentration where the top three clients exceed 25% of recurring revenue can reduce valuation by 10–30%; address it proactively or mitigate it through contract depth.

Where the Premium Is Being Captured Across IT Segments

- MSPs. Median EV/EBITDA reached 11.4x for large-cap transactions in H2 2024 (Aventis Advisors). Sub-scale businesses clear 5–6x on the same profitability. The delta is almost entirely recurring revenue composition, churn profile, and margin quality.

- SaaS. The median private multiple of 4.1x EV/Revenue sits 57% above the all-software median. Vertical SaaS, where workflow integration creates genuine switching costs, accounted for 44% of all SaaS deals in 2024. The Rule of 40 now anchors most serious valuation discussions; growth alone no longer justifies premium multiples without corresponding capital efficiency.

- Cybersecurity. 426 M&A transactions in 2025, up 5% year-on-year, with PE deploying over twice the capital versus 2023 (Momentum Cyber). High-growth vendors above 20% revenue growth are achieving 8.6x EV/Revenue; low-growth peers below 10% are clearing 4.2x (Solganick). MSSPs with contracted recurring service agreements sit at the premium end of that range.

- AI and automation. Multiples here are driven by scarcity and strategic optionality. The transition from bespoke project delivery to platform-based, subscription or usage-based monetisation is the single most value-accretive repositioning available to businesses in this space approaching a sale.

The Window Is Open. Position Matters

Deal volume is recovering, PE appetite is broad, and rate stabilisation has restored the ability to underwrite returns at competitive multiples. For IT business owners weighing the timing of a process, the more relevant question is not whether conditions are at their peak, it is whether the business is positioned to capitalise on them. Recurring revenue quality is the most controllable variable in that equation, and the businesses that get it right consistently extract the strongest outcomes from a competitive sell-side process.

How Merchantec Guides You

Merchantec Capital is an independent corporate finance firm with deep transactional experience across the ICT sector. We work with founders and shareholders of IT software and services businesses at every stage of the M&A process. from initial valuation and revenue quality assessment through buyer identification, process management, and close. Our buyer relationship spans prominent local and international acquirers who are actively mandated to deploy capital into the IT sector, with a particular focus on Software and IT Services businesses exhibiting the recurring revenue characteristics outlined above.

If the dynamics described in this article resonate with where your business sits today, or where you are looking to take it, we would welcome an initial conversation. There are no assumptions around outcomes, and no pressure. Our starting point is simply to understand your ambitions for the business, and to give you an honest view of what the current market could mean for you.